3/9/18 If you’re looking to get out of debt and get your finances in order, then you have to get the 90 Day Budget Bootcamp! This FREE program has transformed the lives of over 65,000 families and walks you step by step through the proven techniques that let you reduce your expenses without sacrificing, create a budget that’s realistic, and a fail proof strategy to actually stick to your budget. Grab it while it’s still FREE here!

Update: 12/21/16 You can now join the 90 Day Budget Boot Camp for free! Get step by step instructions for how to set up a budget, maintain a budget, and save money. With hundreds of success stories and reviews, this is not an opportunity you want to miss! Join the Budget Boot Camp here.

You don’t need complicated, you need easy. You need step by step instructions on how to start a budget that will actually work for you. Done. Grab a seat, a coffee, and a notebook… we have work to do.

Unless you have a healthy cushion in the bank account, it’s not only important to start a budget, it’s important to know when money is going in and coming out. If you skip this step, then you run the risk of overdraft (when you spend more than you have in your bank account and get charged a fee).

This simple way of budgeting solves all of those problems.

There are a million different ways to track your budget, but for right now I want you to be able to do it on paper. This is important. Just trust me on this one. One or two months on paper, and then you can use any online tool or app you want. Stick with me.

One or two months on paper, and then you can use any online tool or app you want. But start on paper.

If you need extensive help on creating and sticking to a budget, the best resource I can give you is the free step-by-step class called “Budget for Beginners Boot Camp” that walks you through not only how to create a budget, but how to set up the basic routines in your life that will support your efforts to save money. Because transforming your finances is about more than just the budget.

You can sign up for the Budget for Beginners Boot Camp class for free by clicking here or entering your email in the box below.

How to Start a Budget: Step by Step.

Step 1: Determine your monthly income.

For some, this is easy- they have consistent paychecks and no additional overtime. They can just add up their paychecks in a month. If you have irregular income, this is enough to create headaches on its own.

If you have irregular income then write down your minimum amount of income this month. This is the amount that you’re very sure you will be making this month.

Example: If you work from home doing data entry and you make anywhere from $1,000- $2,500 every month. Write down $1,000.

If you’re looking for ways to increase you income, you can find the 4 ways I make over $3,000/month as a stay at home mom here as well as a long list of the successful side hustles that will boost your income here.

We’ll deal with your extra income in a few minutes.

Step 2: Create a Monthly Budget Outline.

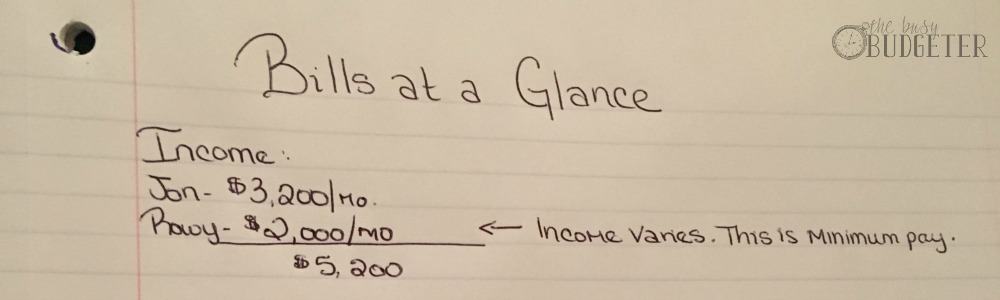

Grab a sheet of paper. Label the top of it with the month and year. On the top of the paper, list the income you just wrote down.

I call that dependable family income. You may make more than that in overtime or more sales, but that’s the amount you feel comfortable relying on.

Now write down your pay dates. I’ll walk you through this using an example of being paid twice a month on the 1st and 15th. List those pay dates on the paper like this:

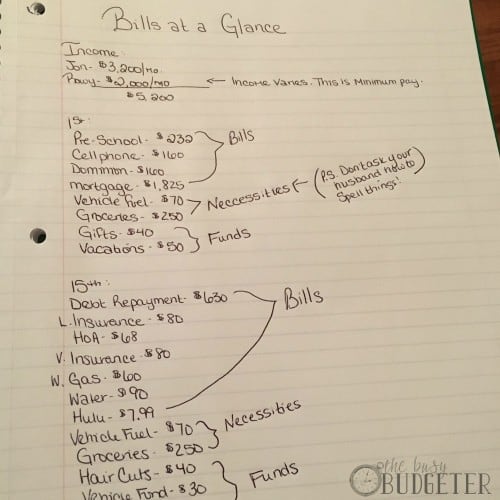

Start to list every bill you have, no matter how small. Separate them by when they are due and list the name and amount due under the 1st or the 15th on your paper.

Step 3: Set a Grocery Budget.

Now decide on a reasonable amount to set aside for groceries. If you’ve never tried to limit your grocery spending, aim high for now and reduce it later. The worst thing you can do is budget one hundred dollars a week, spend three hundred a week then give up.

If you need a basic idea, you can do 15-minute convenience meals at home and spend no more than $120.00 per week, including lunches for two adults (We could feed a small child on that same budget). You can see the menu plan for that here.

Total your groceries and your bills and subtract that total from your total dependable income. Don’t panic if you don’t have a lot of extra money to work with- we’ll work on that next week. This week, just write the numbers down and have an idea where you are now.

What if I have absolutely no idea how much to set aside for groceries?

If you typically use a debit/credit card for all of your purchases- go through the last 30 days of spending in your online bank account and add up the amount for every food-related purchase you made (include eating out).

If it was over $1,000 then shave off 20% and write that number down as your next month’s grocery budget. If that amount is still more than you can afford, you can attempt to shave it down more. However, I would caution that it’s incredibly hard to create lasting change with drastic cuts.

If you’ve been spending $1,600 a month and eating out several times a week, it’s going to be really hard to suddenly go to $500/month because spending $500 a month in groceries involves a ton of new routines. I want to transform your entire life over time. Not drastically cut your spending in a month and then have you relapse into exactly where you are now or worse. Always go for baby steps if you want a change to last.

I want to transform your entire life over time. Not drastically cut your spending in a month and then have you relapse into exactly where you are now or worse. Always go for baby steps if you want a change to last.

Hint: We had the most luck reducing our spending by going through The Grocery Budget Makeover. It’s only available twice a year though. Your best bet is to can get on the waiting list here.

Step 4: Substitute, Substitute, Substitute!

Are there any exchanges you can make that would reduce your bill amounts right now? Look for things that are cheaper but are the same or better than what you’re using1 right now. Here are a few of the most popular examples…

Exchanging Hulu or Netflix for cable.

Straight Talk or Ting for an expensive cell phone plan. (Hint: T-mobile seems to be offering competitive rates as well).

Using the library instead of buying books.

You can read about how we made $23,000 worth of substitutions here.

Choose one bill you can reduce and do it. Call and negotiate a new rate, or make a substitution. Reduce it and then change your list to reflect the new amount.

Your goal in the next few weeks is to continue making substitutions, but leave it at that for right now.

Step 5: Create Funds.

There are quite a few purchases that only need to be made infrequently, like Christmas gifts or vacation. The best way to handle these purchases by creating funds. List these purchases down and set a realistic frequency for which they need to be purchased. Here are a few examples from our funds list:

Haircuts, oil changes, vehicle inspection, vehicle registration, clothes, personal property tax, doctors appointments (if you don’t use flexible reimbursement), gifts, and vacations.

If you have room in the budget, you can add things like entertainment, date nights, kids sports, or even a “good deal” fund into your budget.

The easiest way to save for funds is to open as many bank accounts as needed. We have eight bank accounts for things like “Vehicle Expenses” and “Vacations”. That allows us to put aside a small amount every month to have a large amount available when needed without the risk of keeping cash in the house or the confusion of having everything in one account.

Step 6: Decide about Retirement.

If you don’t already do this, contributing to retirement will be your first goal after creating the budget. We need to set the amount now, though.

In “theory”, it would be smartest to pay off all credit card debt first before you start saving since your return on your investments in unlikely to be as high as interest on your credit card debt. However, if you’re having trouble keeping your finances straight, then forcing yourself to contribute to a Roth IRA (mine through USAA starts at $50.00 per month minimum contribution), forces you to save.

In the event of a true emergency, you can take contributions out (but not profits), and if you take every penny you have and pay off debt, there is no guarantee that you won’t just run up that debt again, undoing all of your hard work.

Start contributing to retirement right now, unless you’re in a unique situation where you’ve already paid off a ton of debt and plan to be debt free in the next few months.

If you contribute to retirement, add this to your budget. (If you contribute pre-tax, there’s no need to add it to your budget).

Step 6: Add in Necessities.

Are there any other things you need to buy every month?

If you drive a car, you’ll need to buy fuel at least monthly. Factor in how much you need to pay for fuel. If you’re not sure, check fuel purchases in your online bank account for the last 30 days.

Determine what your costs are to run your household. Do you ever think of the costs of all the little things needed to run your home? Shampoo, conditioner, body wash, hand soap, laundry detergent, deodorant, light bulbs, batteries, etc? Without being able to predict the cost of these things, a workable budget is a pipe dream. You can head over here and follow the instructions to create a home stock room inventory and price list. Determine the dates that you will stock up (I go for every three months), write down the total cost and the dates of your stock up trips.

If you’re not sure, aim for monthly and then go from there. What do you need right now to run your home for the next month? Shampoo, conditioner, toothpaste, garbage bags, etc. Set an amount monthly to purchase all fo the things you need to run your house and enter that amount into your calendar.

What if I buy all of my groceries and household items together? (Commonly done at Walmart, Costco, and Target?)

Easy! Just combine the categories. Instead of having a “Grocery” and “Home Supplies”, you’ll have “Grocery and Home”.

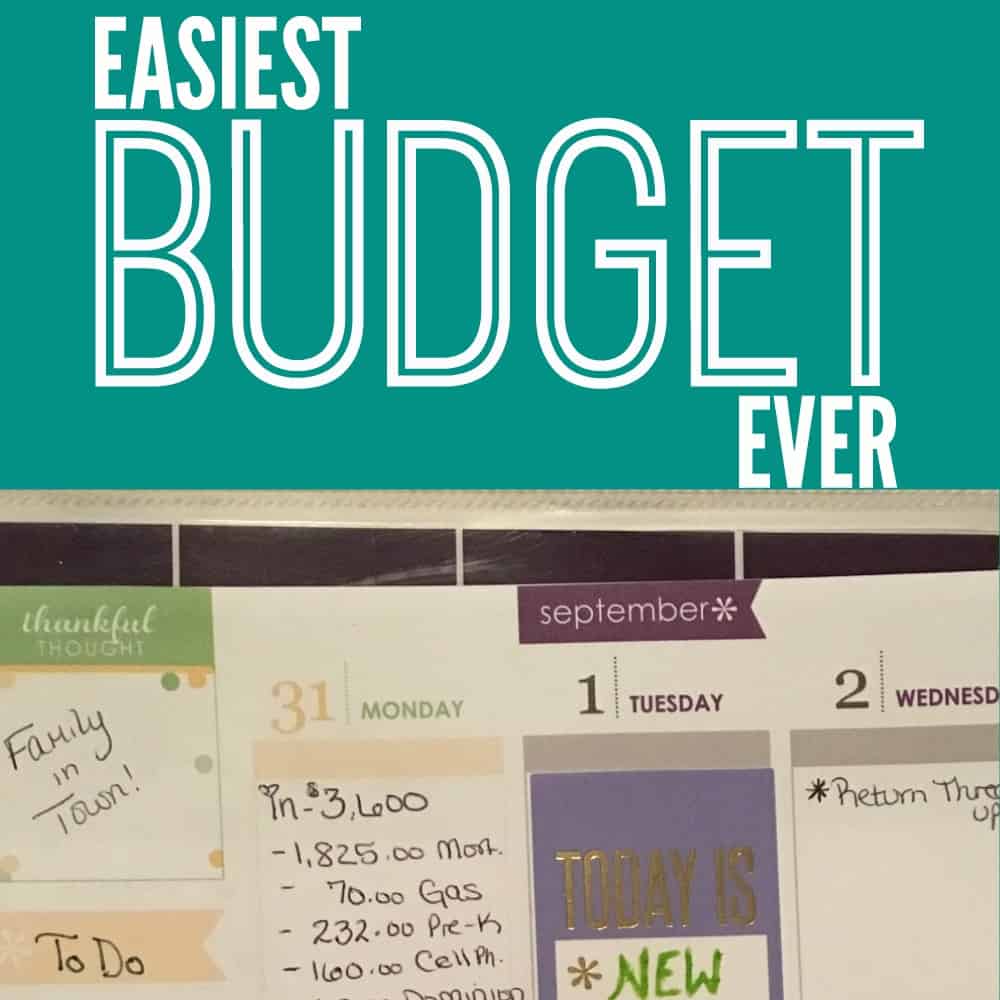

Step 7: Create a Calendar Budget.

Go out and buy a 12-month calendar with giant writing blocks. The one in the photos is an Erin Condren Life Planner, which are gorgeous and popular but pretty expensive. This one from Me & My Big Ideas is AMAZING and way cheaper.

Do the following steps in pencil:

In your calendar…

Write in your pay days, then on your paydays, list the estimated income and list your bills.

Go through your list of necessities and start adding those amounts in on your pay dates preceding the date the money is needed. For gifts, leave at least a month before the event. For instance, my dad’s birthday is on Halloween (October 31st for my foreign readers), so I’m going to list $15.00 on September 1st to buy Dad’s birthday present.

Your budget will be tracked on your payday blocks. If you need additional squares, you can spill over.

Subtract the amounts of each bill/necessity from the income.

What if I don’t have anything left after bills and necessities?

If you don’t have anything left, go back to your lists of bills and necessities and figure out how you can reduce your bills for a while. Cancelling cable is the most bang for your buck, plus it forces you to spend time together and (gasp!) talk to each other!

If you need to make up money, selling things on Ebay is a great option. I’ve done this before and it’s a wild success every time. Take the free selling tutorial first.

Sort through your clothing and grab all of the jeans that don’t fit you and sell them in a lot. Lots of clothing in the same size sell particularly well. Make the listing end on Sunday evening at about 10 pm ET (statistically the most active time for sales).

You can also fill in a small amount with Inbox Dollar earnings, or Ibotta refunds on groceries. You can see more ways to earn additional income here.

The leftover amount each date is your extra income.

Step 8: Goals and the Fun Stuff.

Have you and your family make a list of future goals that cost money. Vacations to Disney World, buying a larger house, opening a brewery, staying home to be with the kids full-time, a new car, living debt free etc. Assign a cost value to each item.

Now think of the smaller goals. Think of things like sending out Christmas cards (that costs money right? most likely it wasn’t in your necessity list), adding a few throw pillows to your living room, getting a new tool for your workshop, visiting your family in Kentucky, etc. Assign a reasonable value to those things. Have each member of the family pick their top 3 priorities.

List the goals in order, 1 being the most important, 3 being the least. Do you see a pattern? Are the same things in the top three? Together determine the family top 3 goals and the order in which they are achieved. For instance, if your goal is to purchase a house, you may want the Disney vacation first, since it will take less time to achieve that goal. Consider alternatives, maybe you would rather vacation somewhere less expensive so you can get the house quicker.

Next determine how strict on the budget you want to be as a family (we choose very strict, with the occasional late night pizza meltdowns). Work together to remind each other of your goals and how to stay on track. Seek other sources of income to create income for additional things that you may want (a blog, an Etsy shop, reselling items on eBay for a profit, etc.)

At the end of each date (the 1st and the 15th), write the first initial for your goal (like H for house), then write the leftover amount. That’s the amount in your “bank” for that goal. If you want to work on a few goals at a time, separate them out and distribute the amount as you please.

Step 9: Update Routinely.

MAKE ABSOLUTELY SURE that you keep track of your actual bank account as well as your bill calendar. If your hubby forgets that he bought something, your bank account will reflect differently than your calendar. Every Monday, review your account online and note any discrepancies from the budget, adjust that date accordingly. Updating daily is even better until you get used to doing it.

I strongly suggest a “cash only” budget if you’re new to budgeting. It takes the guesswork right out of this.

Make your transfer to savings on the last day of the month. I make mine right before bed. I transfer every cent in my checking account over to savings so I start fresh the next day with the new months income.

An added benefit of having your budget in your calendar is that when you check your calendar every day, it automatically reminds you to update your budget. This system works really well with a cash only system.

What’s Next?

Once you’ve worked with this system for a while, we can graduate to an online way to track your budget. You can find my recommendations here, but a pen and paper calendar budget is the best way to start if you’re new to budgeting.

How many times have you started a budget and had it fail?

Other popular posts…

This post may contain affiliate links. If you click & make a purchase, I receive a small commission that helps keep the Busy Budgeter up and running. Read my full disclosure policy here.disclosure policy here.

Original article and pictures take www.busybudgeter.com site

Комментариев нет:

Отправить комментарий